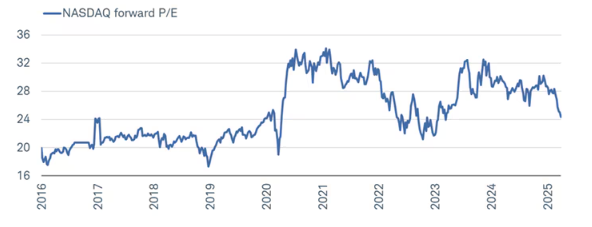

Twenty-five years ago, the dot-com bubble burst, and the NASDAQ reached its peak. Today, we hear the question often in the news: Did AI stocks hit the wall in the first quarter?

Heading into the year, the Magnificent Seven stocks — Apple, Amazon, Google, Meta, Microsoft, Nvidia and Tesla — led the market after carrying much of the heavy lifting over the past two years. Extended valuations in those stocks made them vulnerable to bad news, and they were down about 16% in the first quarter, trailing the broader S&P 500 index. In turn, valuations for NASDAQ stocks have fallen back to levels last seen in early 2023.

Tech and Tech-Adjacent Under Pressure

Investors saw that market diversification was the winner for the first quarter, something we haven’t seen in over three years. In 2022, cash was the only asset class that wasn’t negative, with both stocks and bonds falling more than 15%.

While the average 60/40 portfolio (60% stocks, 40% bonds) was negative for the first quarter, it was down much less than the overall market, thanks to diversification. International stocks, as measured by the MSCI ex-US, were up more than 6% — compared to the S&P 500 being down about 5%. (This was an outperformance by almost 11% for international stocks.)

At the same time, bonds (or fixed income) were positive at almost 3%. The leading sectors in the S&P 500 were healthcare, energy and utilities — not technology.

We believe stocks will remain volatile for the near term, driven mainly by tariffs and uncertainty about policy.

Tariffs are not new, but what is different today is their scale. President Trump is targeting more countries, more aggressively, than he did in his first term.

The U.S. announced permanent 25% tariffs on imported cars and certain auto parts. It is important to remember, however, that this policy can shift rapidly, making the idea of timing the market based on tariff news extremely difficult. Global investors should have some clarity this week, after “Liberation Day” tariff announcements on Wednesday.

The five main goals for Trump’s tariffs are curbing the flow of illegal immigration into the U.S., reducing the flow of fentanyl, leveling the playing field with trading partners, boosting government revenue and boosting domestic manufacturing. Trade policy is evolving, with an emphasis on renegotiated deals to strengthen the supply chain and support American industry.

For decades, the U.S. focused on free trade with its political allies and on allowing consumers access to cheaper goods. This has led to a widening trade deficit, less control over supply chains and declining manufacturing at home.

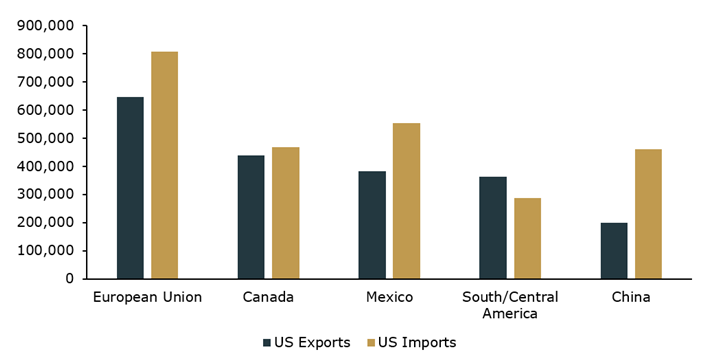

Today the top U.S. exports are energy and autos, while the top imports are autos, auto parts, energy, and electronics. The countries we import from the most to are also the ones that we export to the most, with the notable exception of China, as seen in the chart below.

Imports and Exports by Largest U.S. Trading Partners

Why does this matter?

After decades of prioritizing free trade, U.S. policymakers are focused on strengthening domestic industries and reducing reliance on imports. Tariffs and reworked trade deals are focused on bringing benefits back to the U.S. This is not something that will play out overnight; these moves will take years to implement.

The pandemic highlighted supply-chain disruptions and the vulnerabilities of relying on imports and products that are manufactured overseas. While many corporations have already been shifting manufacturing away from China and other foreign countries, it takes time and money to bring this back home.

This will come at a price for consumers and corporations. Time will tell how this plays out, and we are more than likely to face many more changes to economic policy.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: KIM, Capital Group, Schwab